IRS – Letter 226J

IRS – Letter 226J

What Employers Need to Know

December 4, 2017

Background

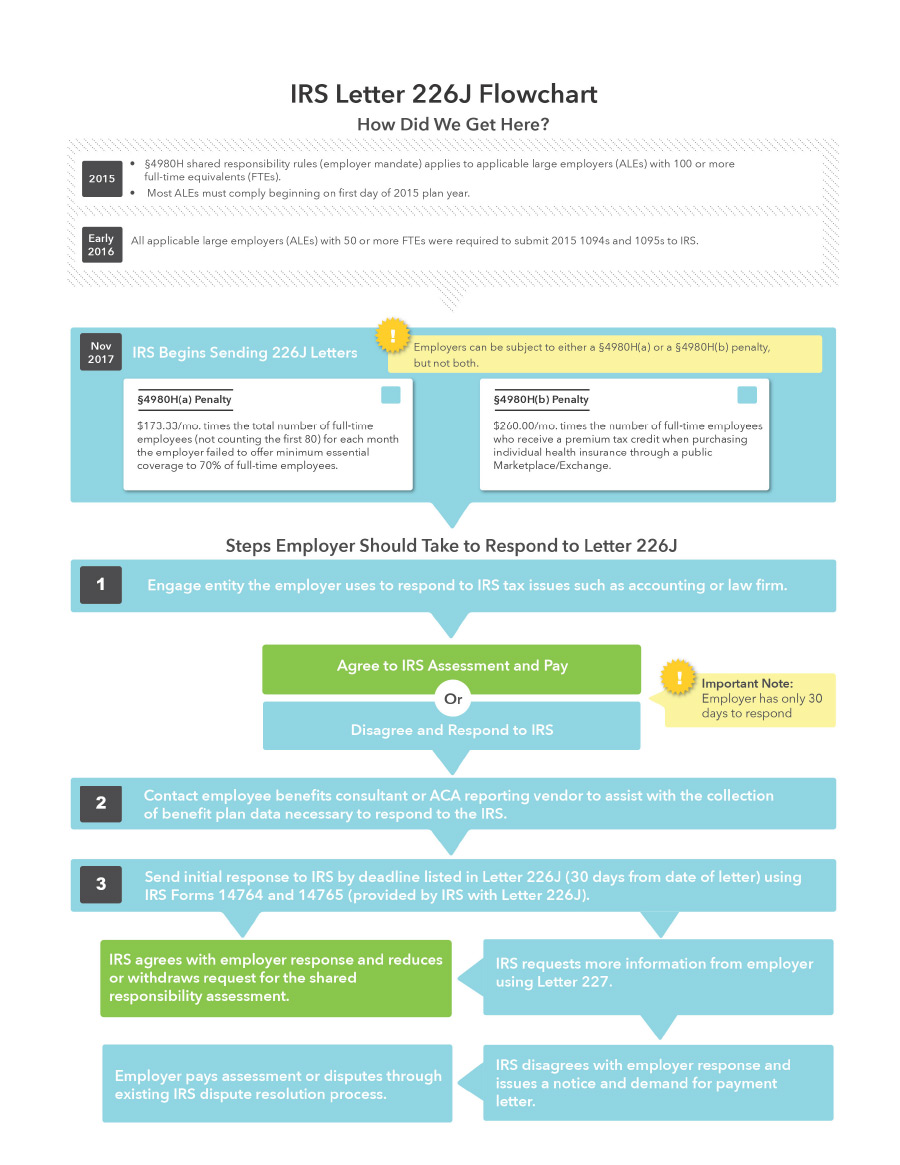

The Affordable Care Act (ACA) contains requirements called the employer shared responsibility rules (often called the employer mandate). Code §4980H requires applicable large employers (ALEs – those with 50 or more full-time equivalents) to offer coverage to full-time employees and their dependent children. Employers who fail to do so face two different potential penalties. The IRS has begun to send letters to employers (Letter 226J) to begin the collection process for employers who have failed to meet the §4980H requirements for benefits offered during 2015. Penalty calculations are based on data provided by employers to the IRS on Forms 1094 and 1095. There are two different penalties that could apply to an ALE, but only one would apply for any particular tax year.

We believe that many of the 226J proposed employer assessments will be applied due to mistakes made in employer reporting, rather than to an actual violation of a §4980H requirement.

§4980H(a) – Offer Coverage to “Substantially All” Full-Time Employees

The so called “(a) penalty” is based on whether the employer made an offer of coverage to enough of their full-time employees. For 2015, an employer who fails to offer minimum essential coverage (MEC) to 70% of all full-time employees (and their dependent children) faces a potential penalty of $173.33/month multiplied by the total number of full-time employees (not counting the first 80). Example of a §4980H(a) penalty:

- An employer with 200 full-time (FT) employees fails to offer coverage to 70% of the FT employees for 9 months of 2015.

- 2015 penalty = $187,196.40

- $173.33 times 120 (FT employees not counting first 80) = $20,799.60 per month times 9 months = $187,196.40

§4980H(b) – Failure to Offer Affordable Minimum Value Coverage

The “(b) penalty” applies if an employer fails to make an affordable offer of minimum value coverage to a full-time employee, and that employee enrolls in individual coverage through a public Exchange/Marketplace and qualifies for the premium tax credit (PTC). For 2015, the (b) penalty is $260/month for each full-time employee who receives a PTC. Example of a §4980H(b) penalty:

- 2 full-time employees are not offered affordable coverage. One receives a PTC for 6 months, the other for 12 months.

- 2015 penalty = $4,680

- Employee 1: $260 times 6 months = $1560; Employee 2: $260 times 12 months = $3120

Receiving Letter 226J

- Alert your mail room to be on the lookout for anything coming from the Department of the Treasury, Internal Revenue Service. With only 30 days to respond or request an extension, you will want the letter forwarded to you immediately.

- Since each employer in an aggregated group was required to file its own 1094 and 1095s with the IRS, ALEs who want to coordinate their response to the IRS should alert all ALE members to be on the lookout for Letter 226J

What an Employer Should Do upon Receiving a Letter 226J

Most importantly, the employer must act quickly. An employer has only 30 days to respond to the IRS. The IRS will initiate a collection process if an employer fails to respond on a timely basis.

- Call the IRS number included on the Form 14764 and request a 30-day extension to respond.

- Contact the entity (accounting firm or law firm) that you use to communicate directly with the IRS for tax-related issues.

- Contact your benefits advisor or firm you used for ACA reporting to help collect data necessary to respond to the IRS.

- See the enclosed flowchart and Q&A for more details on responding to the IRS.

We Can Help

We have access to a team of §4980H and ACA reporting experts ready to help employers understand the Letter 226J and help in developing the employer’s response to the IRS. Fees are based on the complexity of the project and how much time the employer has to respond.

For more information contact your account manager.

Questions & Answers

» What is the IRS process for assessing penalties under the Affordable Care Act?

The IRS has been busy reviewing ACA employer reporting forms filed for plan years that began in 2015. Based on this review, they started sending “Letters 226J” in early November. These letters will go to the individual listed as the contact person on line 7 of Form 1094-C. Some employers will have filed more than one Form 1094-C and will have different contact people listed.

» How do I know if I received a letter from the IRS telling me I owe a penalty under ACA?

Your letter will begin by saying that the IRS has “made a preliminary calculation of the Employer Shared Responsibility payment (ESRP) that you owe.” The letter will probably have a label on the bottom right corner that says “Letter 226J.” It will also include an ESRP Summary Table and Explanation; Form 14764 (“ESRP Response”); and Form 14765 (“Employee Premium Tax Credit (PTC) Listing”).

» What is the first thing I should do if I disagree with the IRS letter?

Your letter will begin by saying that the IRS has “made a preliminary calculation of the Employer Shared Responsibility payment (ESRP) that you owe.” The letter will probably have a label on the bottom right corner that says “Letter 226J.” It will also include an ESRP Summary Table and Explanation; Form 14764 (“ESRP Response”); and Form 14765 (“Employee Premium Tax Credit (PTC) Listing”).

» What is the first thing I should do if I disagree with the IRS letter?

The first thing to do is look at the dates in the upper right corner on the first page of the IRS Letter. The “Response Date” is very important. Failure to respond by this date may result in a demand for payment from the IRS and could make it more difficult to challenge the IRS.

» What are the next things I should do if I plan to pay the penalty?

Just follow the instructions in Letter 226J and include your payment with Form 14764 (You should receive a copy of Form 14764 in your initial letter from the IRS).

» What are the next things I should do if I plan to dispute the penalty?

Consider whether you will engage someone to assist you in dealing directly with the IRS. Who does your organization typically use to respond to IRS tax-related issues? Likely candidates include a lawyer or accountant who can represent you before the IRS. We are prepared to provide assistance regarding benefit plan information to compile the necessary material for you, or your lawyer or accountant, to respond to the IRS.

The views and opinions expressed within are those of the author(s) and do not necessarily reflect the official policy or position of Parker, Smith & Feek. While every effort has been taken in compiling this information to ensure that its contents are totally accurate, neither the publisher nor the author can accept liability for any inaccuracies or changed circumstances of any information herein or for the consequences of any reliance placed upon it.